Shipping supply chains are the backbone of the global economy. The crucial links of this intricate chain stretch across the oceans and seas of the globe. Despite being out of sight and therefore often out of mind, the maritime elements of the network carry ‘over 80 per cent of the world merchandise trade by volume’ The COVID-19 pandemic highlighted the importance of maritime trade and exposed some of the weaknesses of the system. But have these lessons been taken onboard? As geopolitical tensions and the impacts of climate change increase a key question is whether governments are being sufficiently proactive in the management of this critical network or just assuming it will look after itself. This article will look at some of the vulnerabilities of the system and highlight the importance of being proactive.

The commercial shipping industry, made up of over 105,000 ships, is the lynch pin of the global supply chain network. The global fleet carry almost everything including commodities (iron ore, coal, wheat, rice, crude oil) and manufactured goods (cars, computers, food, petroleum products, household goods) across the network of more than 5,000 ports worldwide. The growth of the global population, especially the exponentially growing consumer class, ensures an increasing demand for shipped goods of around 3.2 per cent year on year, meaning the global fleet is expected to number over 130,000 ships by 2030. Whilst ships can get larger, the navigational restrictions of maritime choke points (Panama Canal, Suez Canal, Malacca Straits) and port capacity (length, breadth and vessel draught) are finite and limit vessel size.

Despite the criticality of this industry to us all very few people, outside the industry, understand how it works. This lack of understanding is exacerbated markedly if nations lack an active and current professional maritime community to provide advice at regional and national government levels. This lack of comprehension results in an affliction often referred to as ‘sea blindness’ preventing the crucial proactive preparation and planning for the support of the maritime supply chain.

‘Shipping is inherently global’ from vessel ownership, flag of registration, crew composition, insurance, management and classification with a range of countries. ‘Maritime transport is embedded in a complex global supply chain system in which disruption in one part can rapidly cascade to many others. Ship owners work within a strict economic regime, which the lead maritime economist, Dr Martin Stopford, refers to as the ‘perfect’ market’, with minimal influence by governments who are consumers of the service rather than managers or directors. Shipping is driven by demand despite national or regional loyalties, which is both its greatest strength and potentially its biggest vulnerability.

The capacity of the global commercial fleet is finite because there is little commercial value for individual shipowners to invest in vessel redundancy or spare capacity for emergencies. Whilst it is predicted the global fleet will grow by around 3.2 per cent year on year, this growth is carefully controlled to meet expected demand. Indeed, the shipping industry can benefit significantly when demand unexpectedly increases, as we saw during COVID-19, when the cost of moving goods in a container (referred to as twenty-foot equivalent units or TEU) increased from about USD 2,500 in June 2020 to almost USD 12,000 by September 2021. A combination of increased demand, port congestion, lack of containers and other factors all contributed to increased prices and very long delays. These supply and demand problems were exacerbated when some carriers ‘concentrated on the more profitable … routes and often chose not to call at ports in European or in Sub-Saharan Africa or in Oceania where between 2019 and 2021 container ship port calls saw a double-digit percentage decrease.

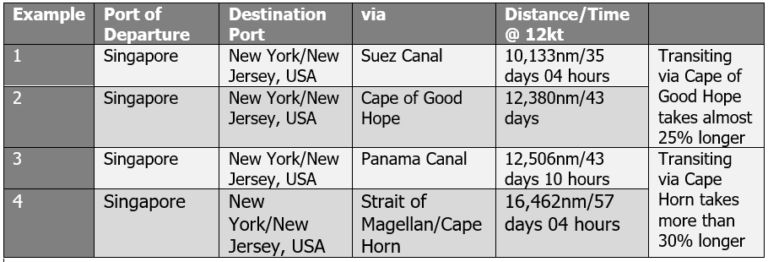

Two recent unrelated series of events have again highlighted these vulnerabilities. The 50 plus attacks on ships by Houthis utilising the Suez Canal (Suez Canal transits, around 26,000 in 2023, have dropped by 42 percent), has pushed many ship owners to avoid the 5,500 nautical mile shortcut and navigate around Africa, adding to the voyage length by several days (see Examples 1 and 2 in Table 1) to a typical voyage at a typical transit speed.

A climate change induced drought in Central America has significantly reduced the water levels in the Panama Canal (Panama Canal transits 13,000 plus per year), restricting the size of ships that can use has reduced its throughput by 49 percent, adding up to 7,000 nautical miles onto voyage lengths around South America; adding as much as 24 days to a voyage from Pacific to Atlantic Oceans (see Examples 3 and 3 in Table 1) and vice versa.

Table 1: Shipping Route/Distance Comparison

All calculations conducted with https://sea-distances.org/

The consequence of these incidents and the longer voyage distances/times will reduce available shipping for charter, pushing up freight rates and could focus carriers on the most profitable routes.

The important lessons from these examples are:

- The shipping network is global, an event in one region of the world can have ramifications across the entire supply chain network.

- Shipping is driven by demand, making less profitable routes more prone to delays and increased freight rates in times of supply chain tension.

- Shipping is driven by market forces.

Whilst these examples are historic in the case of the pandemic and ongoing in the Suez and Panama Canals, they were not foreseen and could not be planned for; and whilst they have placed additional strain on the maritime supply chain, they have not broken it and solutions will be found.

The transition to cleaner fuels

There is however one major change, just over the horizon, that will affect every ship and every port around the globe. The transition to cleaner fuels is going to be potentially as big as the transition from sail to steam. The conversion from sail to mechanical propulsion took more than 100 years, this next change will happen within 30 years. It will require considerable forethought, collaboration, planning and preparation and if not conducted effectively could break the supply chain in numerous places.

To provide some historical perspective it was the introduction of the screw propeller in 1836 that marked the significant change from sail to steam across merchant fleets. The requirement for fire to heat the water to produce steam, also prompted a revolutionary change in ship construction material from wood to steel. Although the first commercial routes were established across the Atlantic by the steel-built ship with a screw propeller, by the SS Great Britain in 1843, neither steam propulsion, nor steel construction were immediately adopted by the shipping industry. Whilst the idea was indeed revolutionary, it was also to an extent experimental, fraught with challenges and critically required the establishment of a global network of coaling ports, where ships could fill their bunkers with the fuel to power the new ships. In 1869, the Suez Canal was opened, significantly reducing the distance between the Atlantic Ocean and the extensive commercial opportunities of the Indian Ocean. However, this required coal to either be carried, by other ships to coaling ports along a shipping route in sufficient quantities to refuel ships or sourced locally in sufficient quantities. Whilst the history of coal mining is global, it was largely used as a fuel to provide heat in homes and was not mined in the industrial amounts to feed steam engines.

Despite its obvious time and distance advantages, the canal was initially not a roaring success, only attracting 500 ships in it first year, as it was ‘foremost a steamship thoroughfare’ largely because transiting the canal and the Red Sea was challenging without alternative propulsion to sails, consequently ‘shipping companies had to adapt to the novelty of a route out East that was almost entirely different to the Cape [of Good Hope] route.’ Traditionally, sailing ships would sail East around the Cape, pick up the ‘roaring forties’ winds launching them towards the trading hubs of India, China and the East Indies, without any need to refuel. Sailing ships continued to be part of the commercial fleet for over 100 years, not inhibited by mechanical failures or the need to replenish coal bunkers, whilst they could compete with their mechanical competitors. The last commercial sailing ship to round Cape Horn was the Pamir in 1949.

Until quite recently, almost all merchant ships used heavy fuel oil, which was the residual fraction in the oil refining process left over when fuels (gasoline, diesel, aviation fuel) have been extracted by refineries. Consequently, heavy fuel oil was considerably cheaper and more widely available. However, this residual black sludge also contained many of the nastier contaminants (sulphur, nitrogen oxides and other toxic gases) found in crude oil, making the emissions from it highly polluting.

On 1st January 2020 the International Maritime Organisation imposed a 0.5 percent sulphur limit on ships operating worldwide. The consequence of this was ships either had to adapt their engines to use a cleaner fuel or retrofit exhaust gas cleaning systems, known as scrubbers, at significant cost (cost of engine conversion/installation of scrubbers and importantly time out of cargo carrying) to limit their emissions and comply with the ruling, so they could enter ports requiring regulatory compliance. There was also a significant logistical challenge, ensuring there was sufficient low sulphur fuels, less globally available than heavy fuel oil, at the 5,000 plus ports across the world to refuel the fleet. To illustrate the scale of the task, a medium sized container ship with capacity for 15,500 twenty foot equivalent units, consumes around 250 tons of fuel per day while travelling at 25 knots. At the United Nations Climate Change Conference COP26 in 2021 there was significant political pressure ‘urging the adoption of sector-wide goal of zero GHG emissions by 2050 and the commercial deployment of zero-emissions vessels by 2030.’ The Marine Environment Protection Committee of the International Maritime Organisation, established in 1985 has been introducing environmental regulations for almost 40 years. The regulatory structure for the shipping industry is well established and is broadly effective. However, the challenges ahead for not only the maritime industry but other stakeholders, including the energy industry, financial industry and logistic enablers are daunting, ‘decarbonizing international maritime transport will require a global perspective.’

A range of 23 new fuels are being designed and manufactured including low sulphur fuels, liquid natural gas (LNG), methanol, liquid petroleum gas (LPG), ammonia (both liquification and internal combustion engines), hydrogen based fuels (Haber Bosch process (nitrogen, hydrogen and heat energy) hydrogen liquification, Fischer-Tropsch (hydrogen and CO2), hydrogen internal combustion engines (ICE) and fuel cells), biofuels and even wind generated power. Opinion is extremely divided across the shipping industry about which fuel(s) are going to be the best for commercial ships and there is no obvious front runner but it is likely that many ships will be duel fuelled initially.

Port of Melbourne, 2016. Credit: Author

Commercial ships spend as much time as possible at sea carrying cargo and earning money. Maintenance periods that require time alongside or in a dry dock are kept to an absolute minimum (planned maintenance/inspections are less than three percent of a ship’s life) as they are non-profitable periods. Ships are expected to have a working life of between 20-30 years, depending on type of cargo carried, operating environment (harsh conditions; heavy seas, polar conditions etc), technological evolution and regulatory compliance.

With a ship’s working life being 20-30 years and the expected implementation of regulations requiring zero emissions compliance by 2050, only 26 years hence, the ship owner’s dilemma is which fuel will be the most cost effective and most widely available so they can decide which type of propulsion engine to purchase in their new ships. As ship owners are private entities this is not a national problem, but understanding which type of ships favour which categories of fuel is very important to all port States.

The dilemma for ports, is potentially much greater, which fuel(s) should they provide, as part of their port services (refuelling or “bunkering” as it is called), if they want to ensure their ports can support the types of ships (tankers, dry bulk carriers, container ships, general cargo ships and passenger liners) they need to attract, so the supply chain for their nation is not interrupted or fails. As part of a nation’s critical national infrastructure, these decisions are crucial and require proactive engagement and planning.

The costs of climate change are going to be considerable and will affect every facet of our lives. Unless governments across the region, especially those at the end of supply chains, actively engage in the decision-making process about the selection and designation of the most appropriate fuels for the ships they depend upon for their export and import trade they are likely to be disadvantaged. The transition to carbon neutral fuels is likely to be fraught with challenges. Access to and acquisition of the fuels may be contested by competing neighbouring states that may aspire to establish hub ports. Different fuels will require appropriate infrastructure to be built at scale to meet demand. When coal was the new fuel for ships, the British Empire was supreme, and the Britannia ruled the waves resulting continued British dominance. Today, the shipping industry is very fragmented without national loyalties and there are many more players in the game. The jeopardy of being at the end or on the periphery of a supply chain requires nations to quickly engage to ensure they are not marginalised.

Peter Cook is an experienced maritime security practitioner. He has worked with intergovernmental agencies (UNODC & IMO), flag and port States, international shipping associations and private maritime security providers across a range of issues. He is an Honorary Fellow with the Australian National Centre for Ocean Resources and Security (ANCORS) University of Wollongong; and is a Visiting Lecturer at City, University of London, and an Associate Member of the Corbett Centre for maritime policy studies at King’s College, London. He is also the Managing Editor of the International Journal of Maritime Crime & Security (IJMCS).

Main image: Ship and sunset in the Gulf of Oman, 2016. Credit: Author.

This article is part of the ‘Blue Security’ project led by La Trobe Asia, University of Western Australia Defence and Security Institute, Griffith Asia Institute, UNSW Canberra and the Asia-Pacific Development, Diplomacy and Defence Dialogue (AP4D). Views expressed are solely of its author/s and not representative of the Maritime Exchange, the Australian Government, or any collaboration partner country government.